Introduction to Personal Budgeting

Personal budgeting is a fundamental aspect of financial management that involves creating a plan for how to allocate income toward expenses, savings, and debt repayment. A budget serves as a guideline to help individuals track their financial activities and make informed decisions. Establishing a budget is crucial for anyone seeking to achieve financial stability and work towards their long-term financial goals.

The importance of a personal budget cannot be overstated, as it offers numerous benefits that significantly improve one’s financial health. Among these advantages, a well-structured budget can greatly reduce financial stress. By clearly outlining income and expenses, individuals can gain better control over their finances, which helps prevent anxiety related to overspending or unforeseen expenses.

Additionally, a personal budget enables individuals to save for specific goals. Whether it is setting aside money for a vacation, purchasing a home, or preparing for retirement, having a budget allows for systematic saving. It encourages individuals to prioritize their spending, ensuring that they allocate sufficient funds to meet both their immediate needs and their long-term aspirations.

A budget also plays a crucial role in avoiding debt. By tracking expenses and adhering to a budget, individuals can mitigate the risk of falling into financial traps that lead to unmanageable debt burdens. With a clear understanding of income and spending habits, it becomes easier to identify areas where one can cut back and avoid unnecessary borrowing.

In conclusion, personal budgeting is an essential strategy for anyone seeking to navigate their financial landscape effectively. It empowers individuals to take charge of their financial well-being, paving the way for a more secure and prosperous future.

Understanding Your Income

Before embarking on the journey of creating a personal budget, it is crucial to have a clear understanding of your income. Accurately identifying all sources of income provides a solid foundation for effective budget planning and helps in making informed financial decisions.

Your primary income typically comes from your job, which can be represented as your gross income—this is the total earnings before any deductions such as taxes, social security, and retirement contributions. However, it is equally important to compute your net income, which accounts for these deductions and reflects the actual amount you receive. Knowing your net income is essential, as it determines how much money is available for monthly expenses and savings.

In addition to your primary employment, consider other potential income streams. For instance, bonuses received from performance incentives can significantly boost your monthly income, as can overtime pay. Furthermore, side jobs or freelance work have become increasingly popular; these can provide valuable supplementary income. Income from investments, rental properties, or dividends should also be included in your calculations, as they contribute to your overall financial picture.

To calculate your monthly income, aggregate all the different sources and ensure that figures reflect a typical month. It may be beneficial to analyze past pay stubs and earnings summaries to ensure accuracy. If fluctuations in income are a factor—common in freelance work, for example—calculating an average based on the past several months can provide a more realistic figure for budgeting purposes.

Understanding your total monthly income, both through a breakdown of various sources and clarification between gross and net amounts, will empower you to develop a comprehensive and effective personal budget that aligns with your financial goals.

Tracking Your Expenses

Tracking your expenses is a critical component of creating a personal budget. Understanding where your money goes each month allows you to identify spending patterns and make informed adjustments. To effectively track your expenses, it is essential to distinguish between fixed and variable expenses.

Fixed expenses include costs that remain constant each month, such as rent or mortgage payments, insurance premiums, and monthly subscriptions. These expenses are predictable and should be relatively easy to account for. On the other hand, variable expenses fluctuate and can include groceries, dining out, entertainment, and shopping. Keeping a close eye on these expenses is vital as they often contribute to budget overflow.

There are various methods to track your expenses, and the choice depends on your convenience and comfort level. Utilizing budgeting apps is one of the most efficient ways to monitor your spending. Many of these apps allow you to link your bank accounts, which enables automatic tracking and categorization of your expenses, providing real-time insights into your financial habits.

If you prefer a more hands-on approach, using spreadsheets can also be an effective solution. By creating a personal budget spreadsheet, you can log your expenses and categorize them to see how much you are spending in each category over time. This method not only allows for personalized adjustments but also enables you to analyze trends in your spending.

For individuals who enjoy traditional methods, manually logging your expenses in a notebook can be beneficial. Regardless of the chosen method, the key is to consistently record your expenditures. Periodically reviewing these records will enhance your awareness of your spending habits, helping you make necessary adjustments to stick to your budget.

Categorizing Your Expenses

Creating a personal budget begins with categorizing your expenses effectively. This is a crucial step, as it allows you to identify what you must spend and where you can cut back. Start by dividing your expenses into broad categories such as housing, groceries, transportation, entertainment, savings, and healthcare. Each of these categories encompasses various subcategories that will help you analyze your financial habits more closely.

Housing is typically one of the largest expenses in most budgets, including mortgage or rent payments, utilities, and property taxes. Next, consider your grocery expenses, which involve not just food but also household supplies. Transportation costs include gas, public transport fares, and maintenance for vehicles.

Entertainment and discretionary spending, although important for a balanced lifestyle, should be viewed separately. This category may include dining out, subscriptions, and leisure activities. Identifying these areas can aid in determining how much of your income should remain available for savings or debt repayment.

Understanding the difference between needs and wants is critical in this categorization process. Needs are items that are essential for survival or well-being, such as food, shelter, and basic healthcare. In contrast, wants are non-essential items that enhance pleasure or comfort, such as designer clothing or frequent dining out. By prioritizing your needs over your wants, you establish a clearer framework for your budget that allows you to focus on financial security first.

Once you have categorized your expenses and understood your needs versus wants, you will have a more structured approach to allocating your funds. This organization assists in effective tracking of your spending patterns and enables better decision-making as you move forward in your budgeting journey.

Setting Financial Goals

Establishing financial goals is a critical first step in creating a personal budget. Financial goals can be categorized into two primary types: short-term and long-term. Short-term goals typically focus on immediate needs and desires, such as saving for a vacation or paying off credit card debt within a year. Long-term goals, on the other hand, often encompass larger aspirations, such as saving for retirement, purchasing a home, or funding a child’s education. Both types of goals are essential as they help guide your budgeting decisions and motivate you to manage your finances effectively.

To begin the process, it is important to reflect on your personal values, lifestyle aspirations, and financial circumstances. Prioritizing your goals is crucial. For example, if you value travel experiences, consider setting a short-term goal to save for an upcoming trip. Alternatively, if creating financial security for your family is paramount, a long-term goal of building a retirement fund might take precedence. Utilize the SMART criteria—goals should be Specific, Measurable, Achievable, Relevant, and Time-bound—to enhance clarity and enhance your chances of success.

Once you have identified and prioritized your goals, it can be beneficial to outline specific action steps for each goal. This may include setting a monthly savings target, creating a dedicated savings account, or reducing discretionary spending in order to reallocate funds towards achieving these objectives. This structured approach not only aids in making your goals more tangible but also keeps you accountable. Tracking your progress regularly will provide insights into your financial habits and help adjust your strategies as necessary. In conclusion, setting well-defined financial goals lays the foundation for a sustainable budget, allowing you to achieve your financial aspirations over time.

Creating Your Budget Plan

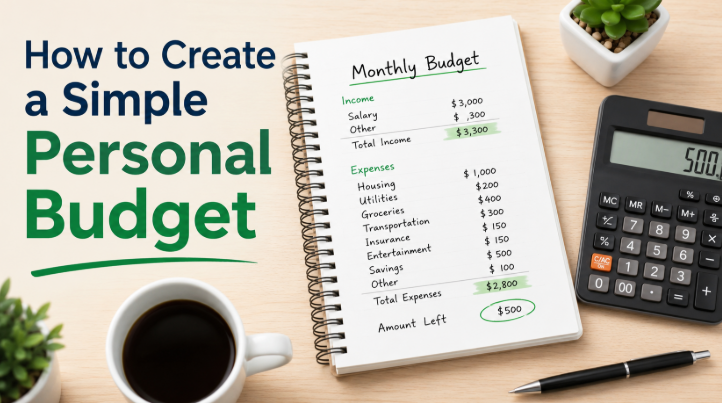

Establishing a personal budget is crucial for maintaining financial health and achieving monetary goals. The initial step in creating an effective budget is to assess your total income, which includes wages, benefits, and any additional sources of revenue. Once you have a clear understanding of your income, it is necessary to categorize and document your expenses. This encompasses fixed expenses like rent or mortgage payments, variable expenses such as groceries and entertainment, as well as discretionary spending.

Among the various budgeting methods available, the 50/30/20 rule is notably popular for its simplicity and ease of use. This approach suggests allocating 50% of your income to necessities, 30% to wants, and 20% to savings or debt repayment. By categorizing income in this manner, individuals can effectively track their spending habits and adjust as necessary. Alternatively, zero-based budgeting entails assigning every dollar of income a specific role, ensuring expenses do not exceed income. This method often suits those who wish to eliminate debt and streamline their financial commitments.

When choosing a budgeting strategy, it is essential to consider your unique financial situation, goals, and spending patterns. For those with stable incomes and fixed expenses, the 50/30/20 rule might prove most beneficial. Conversely, individuals with irregular income or varying expenses may find zero-based budgeting a more suitable option. Furthermore, utilizing budgeting tools or apps can significantly aid in tracking your expenditures and visualizing your financial situation. Whatever method you choose, consistently monitoring and adjusting your budget is key to effectively managing your personal finances.

Monitoring and Adjusting Your Budget

Creating a personal budget is an essential step towards achieving financial stability and meeting financial goals. However, simply developing a budget is not enough; it must be closely monitored and regularly adjusted as circumstances change. Monthly reviews of your budget are typically recommended, allowing you to identify areas where you may be over or under your anticipated expenditures. During these reviews, assess whether your spending aligns with your financial goals, enabling you to make informed decisions moving forward.

In each monthly check-in, compare your actual spending against your budgeted amounts. Consider what categories exceeded expectations and which ones fell short. For instance, if you find that your grocery expenses consistently surpass your budget, it may indicate a need to revise that specific allocation or to enhance your shopping strategies to better align with your financial objectives. Alternatively, if you are underspending in certain categories, those funds could potentially be redirected to savings or debt repayment.

Moreover, life circumstances can necessitate budget adjustments. Significant life changes such as a new job, moving, or a change in family size can heavily influence financial needs. Therefore, it is vital to adjust your budget to reflect new realities. It may also be beneficial to include a “miscellaneous” category to help absorb any unexpected expenses, fostering a more adaptable budget arrangement.

In conclusion, regularly monitoring and adjusting your budget is crucial in maintaining alignment with your financial goals. This practice not only helps in tracking performance versus objectives but also ensures your budget remains relevant as life circumstances evolve. Striving for a dynamic budgeting process will ultimately enhance your financial well-being.

Common Budgeting Mistakes to Avoid

Creating a personal budget is a vital step towards financial stability and success; nonetheless, many individuals encounter common pitfalls that hinder their budgeting efforts. One of the most significant mistakes is underestimating expenses. Often, essential costs such as utilities, groceries, and transport can exceed initial projections, leading to budget deficits. Therefore, it is prudent to track past expenses meticulously and incorporate a cushion for unforeseen costs to enhance the accuracy of budgeting.

Another frequent error is the failure to adapt to changes in financial circumstances. Life is dynamic, and changes such as job loss, new employment, or unexpected medical expenses can significantly impact one’s financial situation. Failing to review and adjust a budget periodically can result in unrealistic financial planning, making it essential to revisit the budget regularly to account for these changes and maintain financial health.

Neglecting savings is also a common budgeting misstep. Many budgets focus solely on immediate expenses and overlook the importance of setting aside funds for future goals or emergencies. Establishing a dedicated savings category within a budget ensures that individuals are financially prepared for unexpected events and can pursue long-term objectives such as homeownership or retirement. Implementing the “pay yourself first” strategy can assist in prioritizing savings before allocating funds to other expenditures.

To avoid these mistakes, individuals should embrace a proactive approach to budgeting. Regular expenses tracking, continual adjustment to changing circumstances, and an emphasis on savings can build a more robust financial strategy. By steering clear of these common missteps, individuals will enhance their budgeting discipline, paving the way for a healthier financial future.

Conclusion and Next Steps

Establishing a personal budget is a fundamental step toward achieving financial stability and fostering a secure economic future. A budget not only helps in tracking income and expenses but also empowers individuals to make informed financial decisions that can lead to increased savings and reduced financial stress. By sticking to a budget, one can allocate resources effectively, prioritize needs over wants, and ultimately work towards financial goals.

To further enhance your financial literacy and develop more robust budgeting habits, consider engaging in various educational activities. Reading books on personal finance can provide valuable insights and tips on effective budgeting strategies. Authors such as Robert Kiyosaki and Dave Ramsey have published works that delve into financial education, providing advice that can transform your approach to managing money.

Additionally, attending workshops or seminars focused on budgeting and financial planning can offer practical guidance and foster a deeper understanding of budgeting concepts. Many financial institutions and community programs offer these resources, giving you the opportunity to learn in a collaborative environment.

Utilizing financial planning tools and mobile applications can also streamline your budgeting process. Numerous tools are available that allow you to track transactions in real-time, set spending limits, and analyze your financial behavior. Choosing the right tools can lead to greater adherence to your budget and help maintain motivation in your financial journey.

In summary, taking actionable steps towards effective budgeting can significantly improve one’s financial status and contribute to overall well-being. Embrace the process, continue learning, and remain committed to refining your budgeting skills for sustained financial health.