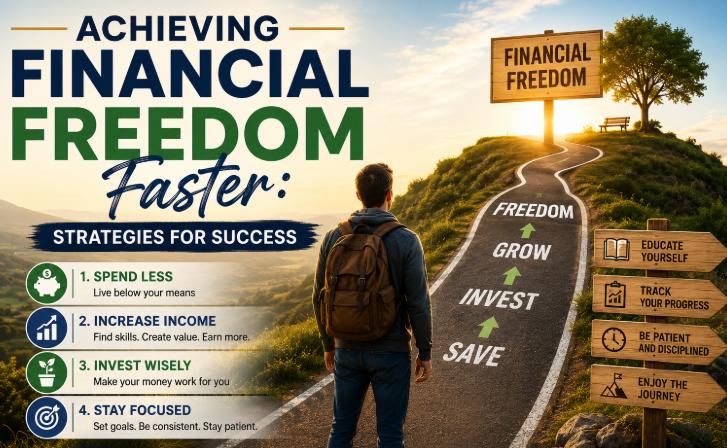

Understanding Financial Freedom

Financial freedom represents the state whereby an individual has sufficient personal wealth to live without having to actively work for basic necessities. It is characterized by having enough income or financial resources to support one’s lifestyle and cover future expenses. The key components of financial freedom include debt elimination, savings and investment, diversified income streams, and a robust financial plan. Achieving financial independence entails not only having substantial wealth but also the ability to make choices that enhance one’s quality of life without being hindered by financial constraints.

The importance of financial freedom cannot be understated. It allows individuals to live life on their terms, pursue passions, and enjoy leisure without the constant worry of financial obligations. Moreover, achieving financial independence transforms how one approaches work and opportunities. Instead of working solely for survival, individuals can engage in vocations they are passionate about, which can lead to greater job satisfaction and overall well-being. This liberation also grants the freedom to make investments in personal health, education, or travel, further enriching life experiences.

A crucial aspect of obtaining financial freedom is cultivating a mindset geared towards saving and investing. It requires individuals to shift their perspectives towards wealth accumulation and long-term financial planning. This might involve embracing frugality, being intentional with spending, and prioritizing investments over instant gratification. Furthermore, individuals aspiring for financial independence should foster resilience and adaptability, remaining open to learning new strategies and approaches to enhance their financial situation. Building this mindset is fundamental, as it empowers individuals to navigate challenges effectively on their journey towards achieving financial freedom.

Setting Clear Financial Goals

Establishing clear financial goals is a critical first step toward achieving financial freedom. By identifying your aspirations and outlining a plan to reach them, you create a framework that motivates and directs your financial decisions. The SMART criteria, which stands for Specific, Measurable, Achievable, Relevant, and Time-bound, is an effective tool for formulating these goals.

When formulating your financial goals, it is essential to be specific. Vague goals, such as “I want to save more money,” can lead to confusion and lack of direction. Instead, define an exact amount, such as “I want to save $10,000 over the next two years.” This specificity helps clarify the action steps needed to achieve your target.

Measurable goals allow you to track your progress objectively. Setting milestones, such as saving $2,500 each six months, enables you to assess whether you are on track to meet your ultimate goal. Regularly revisiting these benchmarks provides an opportunity to adjust your plans if necessary, ensuring you remain focused on your path to financial freedom.

Moreover, it is crucial to ensure your goals are achievable. While it is beneficial to challenge yourself, setting unattainable targets may lead to frustration and a sense of failure. Consider your current financial situation; set realistic goals that stretch your capabilities but remain within reach.

Relevance is also a vital aspect of goal-setting. Each financial goal should align with your long-term vision and values. For instance, if long-term security is your priority, goals associated with retirement savings should take precedence.

Lastly, applying a time-bound element to your goals instills a sense of urgency. Specify when you aim to achieve each goal, as this enhances motivation and fosters accountability. By setting clear timelines, you create a structured approach to reaching your financial objectives. Implementing these strategies will significantly enhance your financial planning process, making it more effective and aligned with your aspirations.

Creating a Budget That Works

Developing a personalized budget is a fundamental step toward achieving financial freedom faster. A well-structured budget helps individuals outline their income, expenses, savings, and investments, providing a clear view of their financial situation. To create a budget that works effectively, start by calculating all sources of income. This includes salary, side hustles, and any other sources of revenue. Understanding your total income sets the groundwork for your budgeting journey.

Next, it is crucial to track spending habits meticulously. This can be achieved by maintaining a log of all expenditures over a specified time period, allowing for identification of where money is being spent. Categorizing expenses—fixed (like rent or mortgage) and variable (such as dining out or shopping)—can reveal patterns and areas where adjustments can be made. By assessing these categories, you can pinpoint unnecessary costs that can be eliminated or reduced, facilitating a more streamlined budget.

Once income and expenses are clearly defined, allocate funds appropriately toward savings and investments. It is generally advisable to adopt the “50/30/20” rule—50% of your income towards needs, 30% towards wants, and 20% towards savings and debt repayment. This framework provides a balanced approach and can be personalized to suit individual financial goals. Furthermore, consider automating savings by setting up regular transfers to savings accounts. This makes it easier to prioritize saving without the temptation to spend that money.

Incorporating regular reviews of your budget will ensure that it evolves in response to changing financial circumstances. A successful budgeting strategy is consistent and flexible, enabling you to adapt your financial plan as needed. By adhering to these principles, you will be on your way to creating a budget that not only works but also supports your journey toward financial freedom.

Increasing Income Through Multiple Streams

In today’s economic landscape, relying on a single source of income may not be sufficient to achieve financial freedom. The concept of diversifying income sources has gained momentum, as individuals seek innovative ways to increase their financial stability. Establishing multiple streams of income can provide security against unexpected financial changes, such as job loss or economic downturns.

One effective strategy is to explore side hustles. These side jobs often leverage an individual’s existing skills or interests, allowing them to monetize hobbies such as photography, writing, or crafts. In addition to offering additional income, side hustles can serve as a valuable platform for personal growth and exploration of entrepreneurial ideas.

Another noteworthy avenue is passive income, which is income earned with little to no ongoing effort. This may include investments in stocks, rental properties, or creating digital products such as e-books or online courses. Such ventures not only generate money but also create financial assets that can grow over time, further reinforcing one’s financial security.

It is essential to identify skills that one possesses and recognize how they can be transformed into income-generating activities. For example, someone with expertise in a specific field may consider consulting or freelancing, while another with a knack for teaching can create online tutorials. Exploring various income avenues can be both rewarding and financially advantageous.

Ultimately, diversifying income sources is not merely a strategic choice; it is becoming a necessity for individuals who aspire to attain financial freedom. By embracing the concept of multiple streams of income, one can enhance their financial situation, reduce risk, and build a more secure future.

Investing Wisely for Long-Term Growth

A critical component of achieving financial freedom is investing wisely, which can pave the way for long-term growth. Various investment vehicles are available, each with its own set of risks and rewards that need careful evaluation. Stocks, for instance, represent ownership in companies and can provide substantial returns over time. However, they also come with increased volatility, necessitating a solid understanding of market trends and individual company performance.

On the other hand, bonds are deemed safer investments, as they typically offer fixed interest payments over a specified period, returning the principal amount upon maturity. While they may not yield as high returns as stocks, incorporating bonds into an investment portfolio can create a balance between risk and stability.

Real estate is another viable option, allowing investors to capitalize on property appreciation and rental income. This asset class requires an understanding of market conditions, location desirability, and property management, but can be an excellent hedge against inflation while diversifying an investment portfolio.

A crucial aspect of investing is risk assessment; understanding your risk tolerance is essential in crafting an investment strategy that aligns with your financial goals. Younger investors may opt for a growth-oriented strategy emphasizing equity investments, while those nearing retirement may favor a more conservative approach, focusing on income-generating investments.

Additionally, the power of compound interest cannot be underestimated in the path toward financial independence. This principle entails earning interest on both the initial investment and the accumulated interest over time, exponentially increasing wealth. The earlier one starts investing, the more pronounced the effects of compounding become, making time a vital ally in the journey toward financial freedom.

The Power of Saving and Emergency Funds

Saving is a cornerstone of achieving financial freedom, serving as a buffer against unforeseen circumstances and providing peace of mind. The first step in this journey is to establish a solid saving habit. However, for this savings to be effective, it is essential to differentiate between saving and investing. While saving typically refers to setting aside money for short-term needs, investing involves allocating money with the expectation of generating a return over the long term.

Building an emergency fund is a crucial component of effective saving strategies. An emergency fund is designed to cover unexpected expenses, such as medical emergencies, car repairs, or job loss. Financial experts recommend aiming for three to six months’ worth of living expenses. To begin constructing this fund, consider starting small; set a manageable monthly savings goal and gradually increase it as your financial situation improves. Utilizing high-yield savings accounts can also maximize interest earnings while keeping your funds accessible.

To develop consistent saving habits, it is beneficial to automate savings. This can be achieved by setting up automatic transfers from your checking account to your savings account right after payday. This technique not only ensures that you save a portion of your income every month but also reduces the temptation to spend that money unnecessarily. Additionally, consider setting up specific saving goals, such as travel, education, or even retirement, which can motivate you to stick to your saving plan. Adopting theses habits now can significantly enhance your path toward financial independence and ensure that you’re well-prepared for unexpected financial challenges.

Reducing Debt and Managing Credit

Debt can be a significant barrier to achieving financial freedom, making effective management of this burden crucial. A popular method for addressing debt is the snowball approach, which entails paying off the smallest debts first. As each small debt is eliminated, the individual gains psychological momentum, which can help in tackling larger debts subsequently. This method provides a sense of accomplishment that encourages individuals to continue their debt repayment journey. Alternatively, the avalanche method focuses on paying off debts with the highest interest rates first, ultimately saving money on interest payments. This tactic may be more beneficial for those who prioritize minimizing the total interest incurred over the method’s psychological boost.

Establishing a budget can also facilitate effective debt repayment. By determining necessary expenses and allocating a portion of income specifically towards debt reduction, individuals can better prioritize their financial obligations. It is essential to regularly review this budget to identify possible adjustments that can lead to further financial savings.

Managing credit is equally important in the quest for financial independence. A substantial credit score can open doors to better financing options and lower interest rates, making future borrowing more manageable. Regularly monitoring credit reports is an effective practice to ensure that all information is accurate and up to date. Addressing any inaccuracies can significantly improve one’s credit standing.

Additionally, maintaining healthy credit practices, such as making timely payments and keeping credit utilization ratios low, is vital in bolstering a credit score. These actions not only enhance creditworthiness but also strengthen overall financial health. By effectively reducing debt and managing credit, individuals are more likely to achieve their financial freedom goals earlier than anticipated.

Staying Motivated and Overcoming Roadblocks

The journey toward financial freedom is often marked by obstacles that can hinder your progress and erode your motivation. Common challenges include unexpected expenses, fluctuating income, or a lack of immediate results, which can lead to frustration and self-doubt. To navigate these hurdles effectively, it is crucial to develop strategies to maintain your motivation and resilience.

One effective method to stay motivated is to set clear, achievable financial goals. Break larger objectives into smaller, manageable milestones that can provide a sense of accomplishment as you reach them. Documenting your progress not only helps track your advancements but also serves as a visual reminder of your commitment to attaining financial freedom. Celebrate each small achievement alongside your significant milestones to sustain enthusiasm and momentum throughout your journey.

Moreover, adopting a growth mindset can significantly enhance your ability to overcome challenges. Embrace setbacks as opportunities for learning and growth. Reflect on what went wrong, identify the necessary adjustments, and adapt your strategies accordingly. This resilient approach not only fosters perseverance but also keeps you focused on your long-term objectives.

Surrounding yourself with a supportive community can also be highly beneficial. Engage with like-minded individuals, whether through online forums, social media groups, or local meet-ups, who share similar financial aspirations. Sharing experiences and receiving encouragement from others can reinforce your motivation and provide you with newfound perspectives on overcoming challenges.

Additionally, developing positive affirmations about your financial journey can help reframe your mindset. Regularly remind yourself of your capabilities and the significance of your goals. Keeping a journal focusing on both your achievements and aspirations is another effective technique to maintain a positive outlook.

In conclusion, navigating the roadblocks to financial freedom requires a strong sense of motivation and resilience. By setting achievable goals, adopting a growth mindset, seeking community support, and fostering positive affirmations, you can effectively overcome challenges and remain focused on your financial objectives.

Reviewing and Adjusting Your Financial Plan

Achieving financial freedom is a dynamic process that requires ongoing attention and flexibility in one’s financial plan. Regularly reviewing and adjusting this plan is essential to ensure that it remains aligned with individual goals and circumstances, which can change over time. As one’s financial situation evolves, whether due to a change in employment, unexpected expenses, or shifts in investment performance, adapting the financial strategy will help maintain the path toward financial independence.

To begin, tracking progress is crucial. Individuals should regularly assess their financial standings, which includes reviewing income, expenses, and investments. This allows for a clear view of whether one is on track to meet established financial goals or if adjustments are needed. Periodic makeovers of the budget can unveil areas where spending may be reduced or savings can be maximized, making it easier to achieve financial targets more efficiently.

In addition to tracking progress, it is also important to reassess goals periodically. Initially set financial objectives may no longer be applicable as life circumstances change. For example, a desire for early retirement may adjust to include the need for children’s education funding or a change in lifestyle aspirations. By revisiting and recalibrating goals, one can ensure that their financial plans remain relevant and achievable.

Finally, making the necessary changes in strategies is vital. This could involve reallocating assets, exploring new investment opportunities, or even consulting with financial advisors for expert insights. Adjustments to a financial plan may be required to account for fluctuating markets, personal passions, or innovative saving techniques. Through consistent evaluation and realignment of one’s financial framework, moving towards financial freedom becomes a more structured and actionable endeavor.